Silicon Valley Real Estate Market Update: December 2024 Insights and Analysis

Kevin Swartz | December 23, 2024

Market Update

Kevin Swartz | December 23, 2024

Market Update

Quick Take:

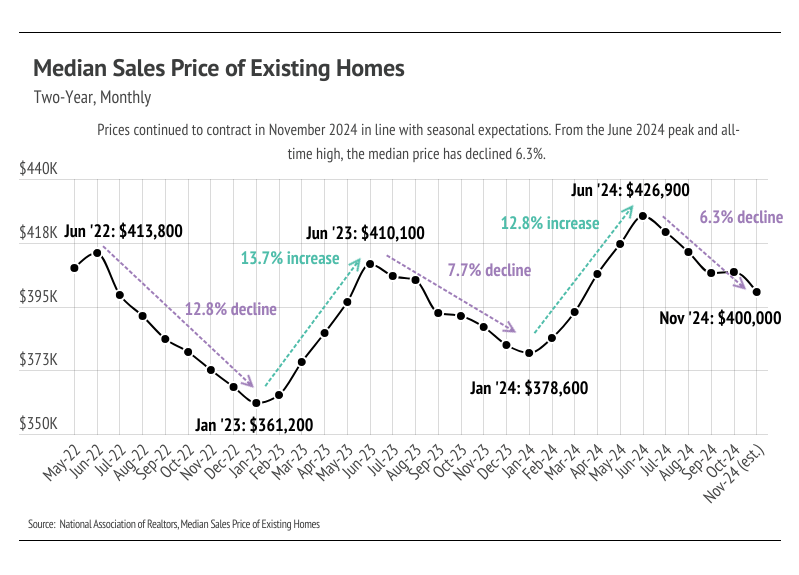

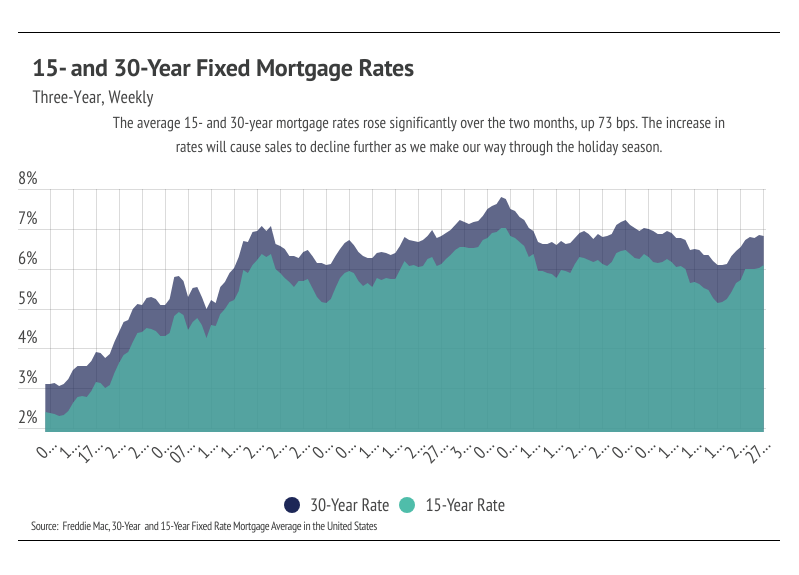

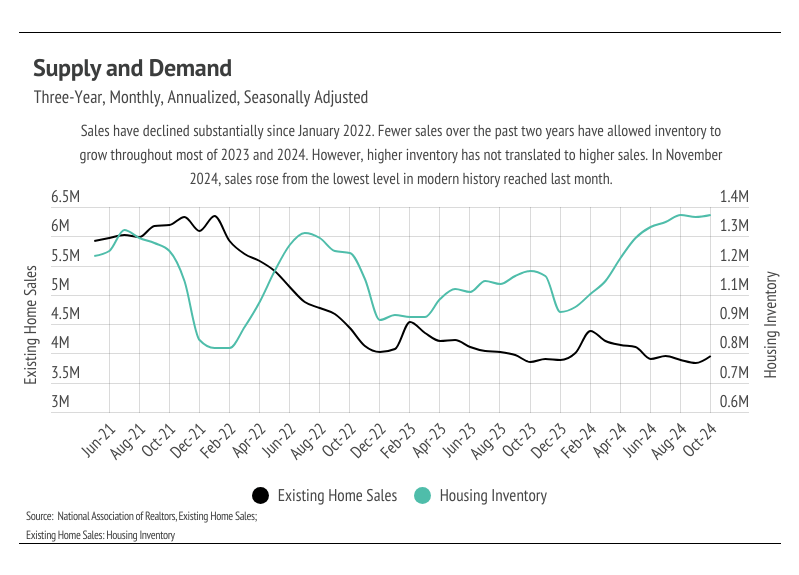

The 2024 housing market was marked by low sales volume, rising inventory, elevated mortgage rates (6.73% on average in 2024), and record high home prices. Low sales volume is easily explained with the combination of high prices, high rates, and the buying boom that happened from June 2020 to June 2022. Record high prices along with a high mortgage rate not seen in 20 years priced buyers out of the market. In June 2024, the median home price reached an all-time high of $426,900 and has since decreased to $400,000, which is in line with the normal seasonal contraction expected in the second half of any calendar year. The all-time high median home price coincided with mortgage rates averaging 6.92%, which equated to the highest monthly mortgage payment ever. Since June, the median home price has declined 6.3%, and we expect prices to continue to decline in December 2024 and January 2025 — the normal seasonal pattern.

As we close out 2024, the economy is doing well by just about every economic metric we typically use: strong job growth, low unemployment, lower inflation, and positive real GDP,to name a few. Interest rates have stayed elevated, which makes the cost of borrowing money higher and, in a sense, slows the economy.. However, even though interest rates have remained higher, the economy hasn’t slowed much while inflation has declined, which was the Fed’s desired effect. As we look forward to 2025, there isn’t much choice but to consider the anticipated economic effects that may come with the administration change.

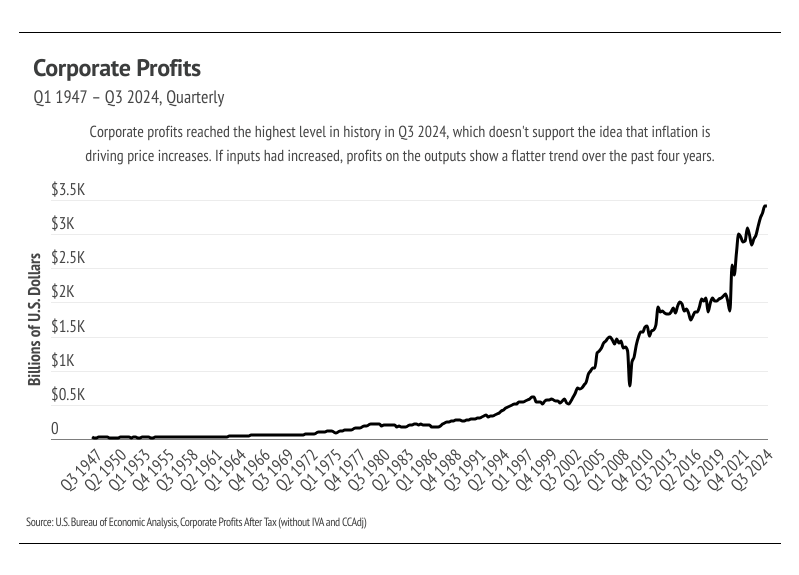

Since last month’s letter, the incoming Trump administration’s stated economic policies haven’t wavered, so tariffs on at least three major trade partners — China, Mexico, and Canada — could go into effect in early 2025. Tariffs raise the price of goods for the importing country and, as corporate profits show, corporations are not willing to accept any downturn in their profits. In Q3 2024, corporate profits reached the highest level in history. For better or worse, we live in a global economy, and the U.S. is a net importer of goods, so corporations will increase prices to offset the tariff (tax) on the goods they import. The U.S. auto industry is particularly vulnerable to tariffs. If car prices rise by 25% almost overnight, sales will drop, causing a spiral of layoffs. Fresh produce is a major agricultural import for the U.S., especially from Mexico and Canada, so food will become more expensive after the tariffs. At the same time, immigrant labor is the backbone of U.S. agriculture and construction, which could be affected by new immigration policies. During Trump’s interview with Kristen Welker, he did not guarantee that tariffs won’t raise prices for the American people — because prices will rise. With inflation comes higher interest rates, so we believe, at best, that mortgage rates will stabilize around 6.5%. At 6.5% interest, a mortgagor pays 32% more per month than the same mortgage at 4%, meaning that fewer buyers will be in the market with a higher interest rate.

In short, there is a high probability that goods and construction costs will become significantly more expensive and that the U.S. will experience a labor shortage in agriculture and construction. Broadly, home prices will probably remain stable in the coming year with lower price growth than we’ve seen in the past four years, but new construction costs could dramatically increase along with delays from fewer workers.

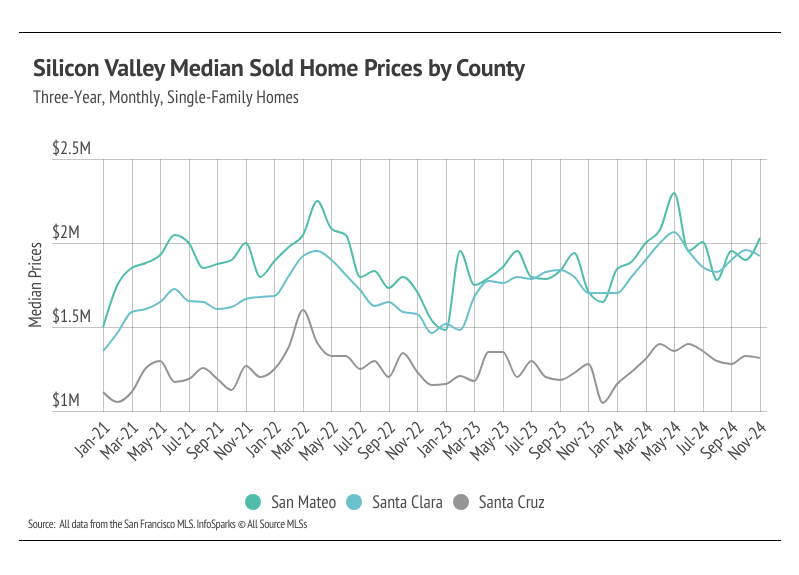

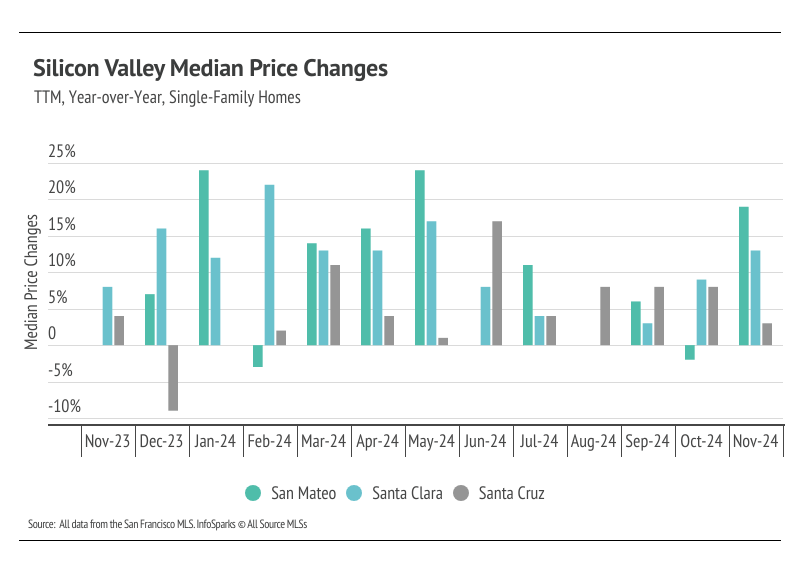

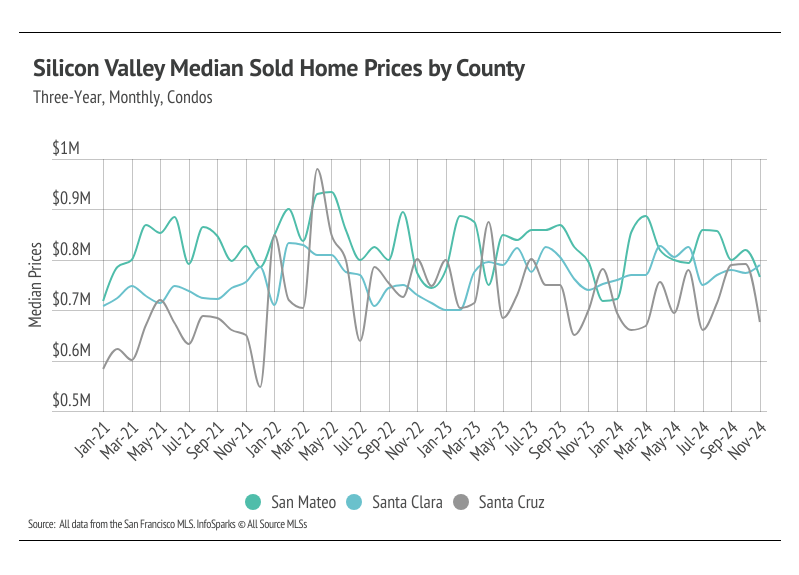

Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage for your area. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

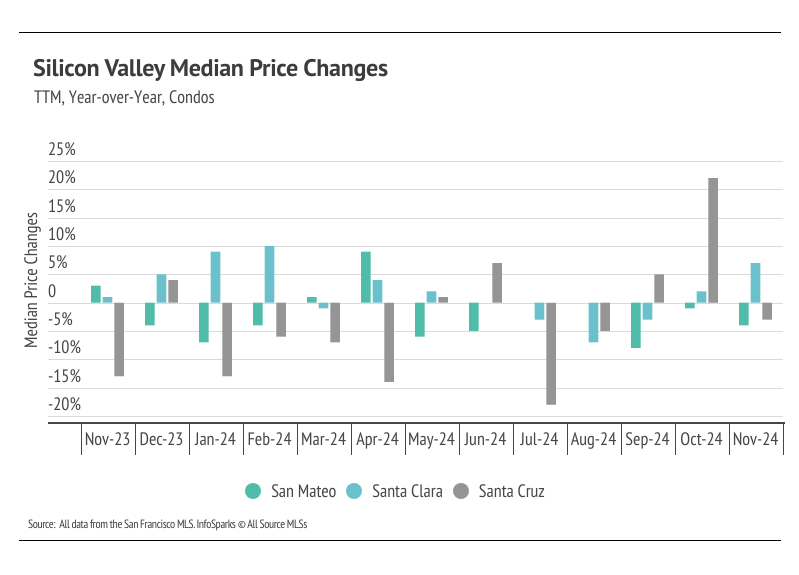

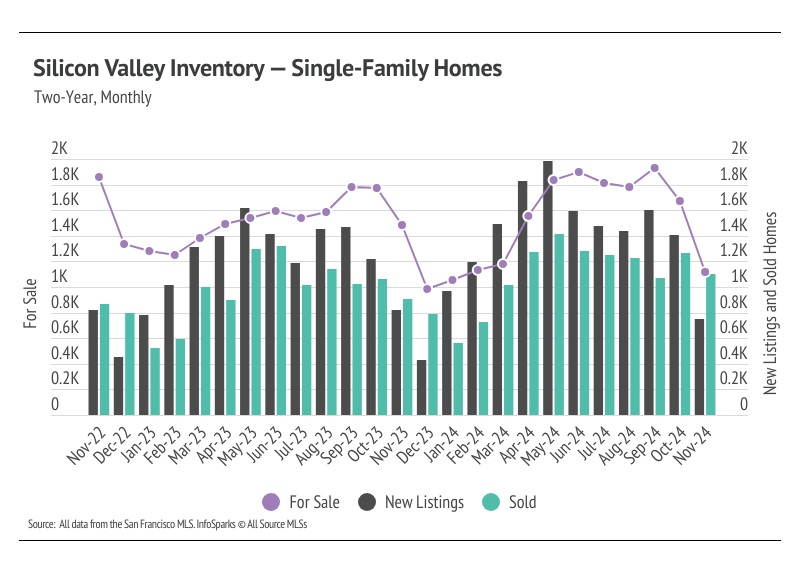

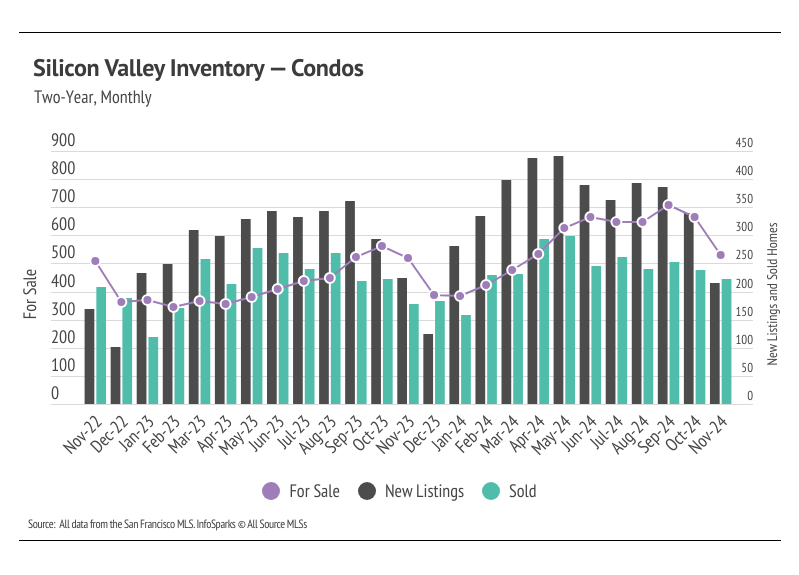

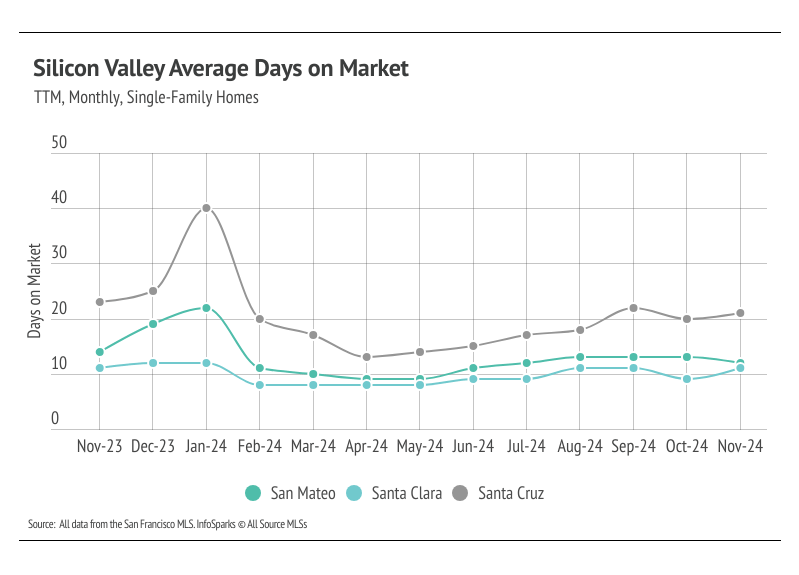

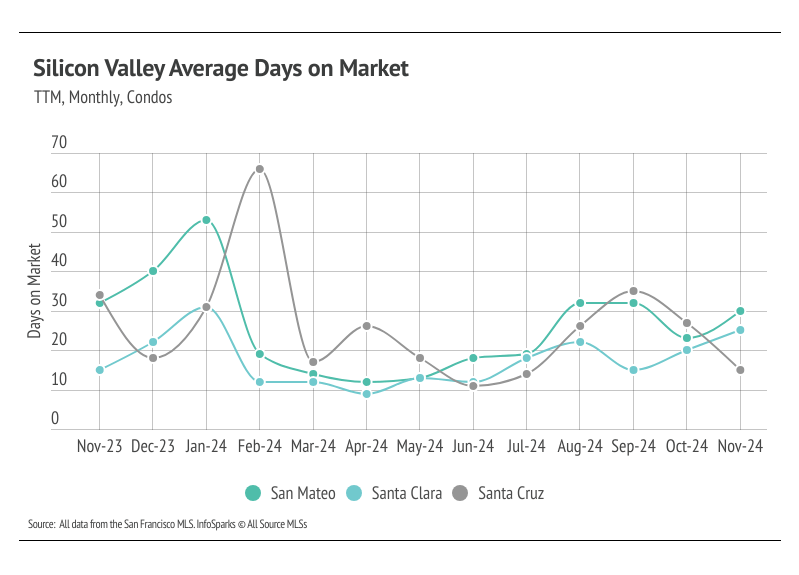

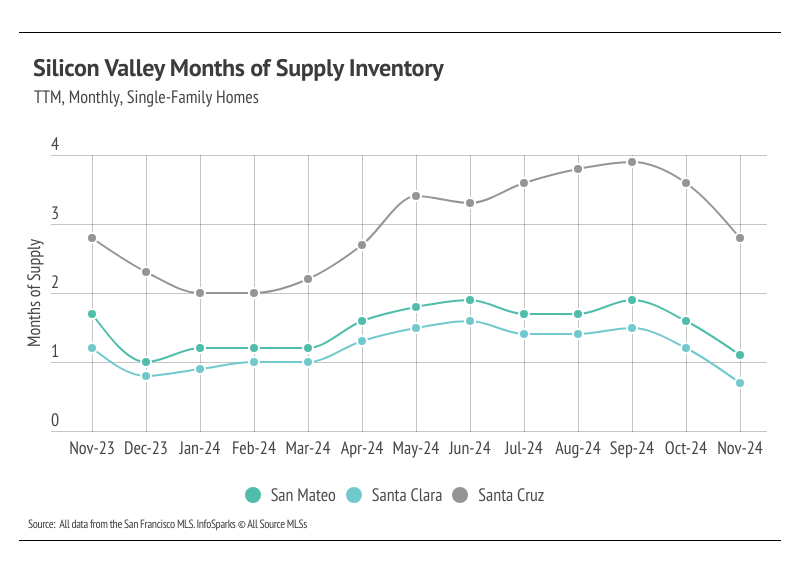

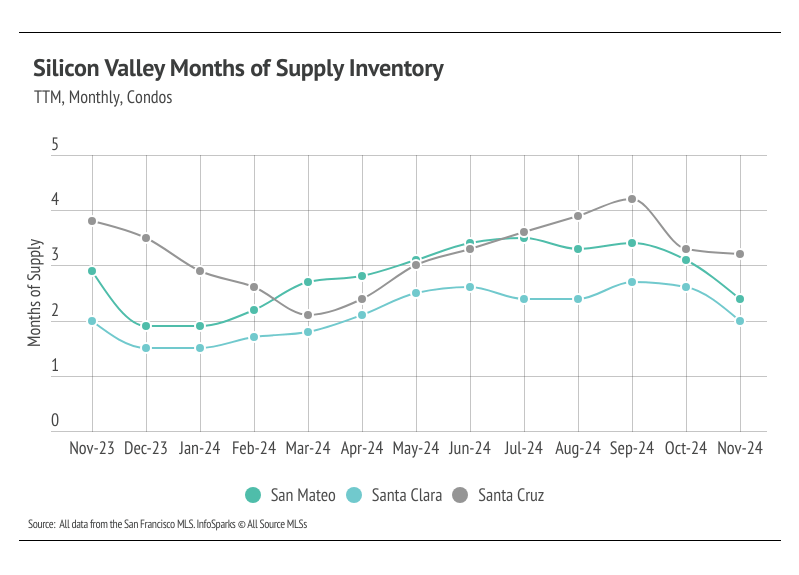

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). The Silicon Valley market tends to favor sellers, which is reflected in its low MSI. In 2024, Silicon Valley MSI moved higher, particularly in Q2. In October and November, MSI dropped across markets. MSI indicated a sellers’ market for single-family homes and condos with the exception of the Santa Cruz condo market, which is more balanced.

Trends, prices, and insights shaping Silicon Valley housing this winter

Trends, prices, and insights shaping Silicon Valley housing this fall

You’ve got questions and we can’t wait to answer them.