Silicon Valley Real Estate Market Update: April 2024 Insights and Analysis

Kevin Swartz | April 19, 2024

market update

Kevin Swartz | April 19, 2024

market update

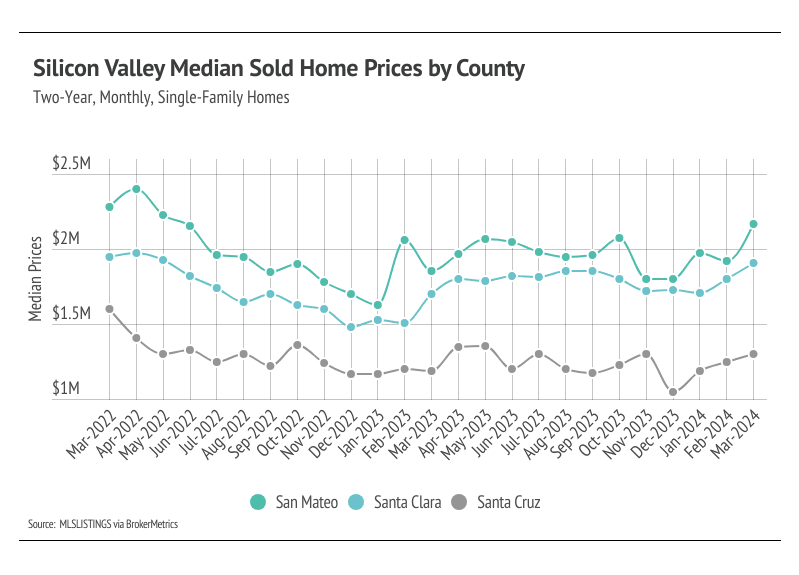

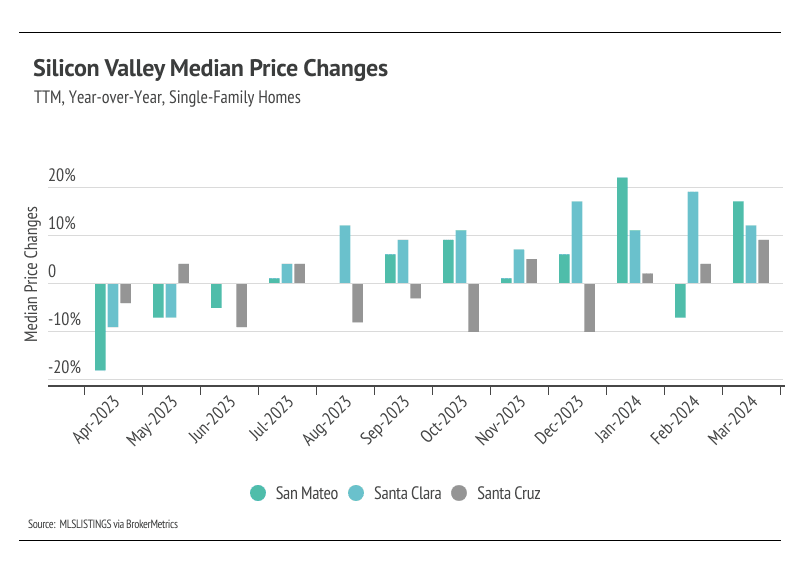

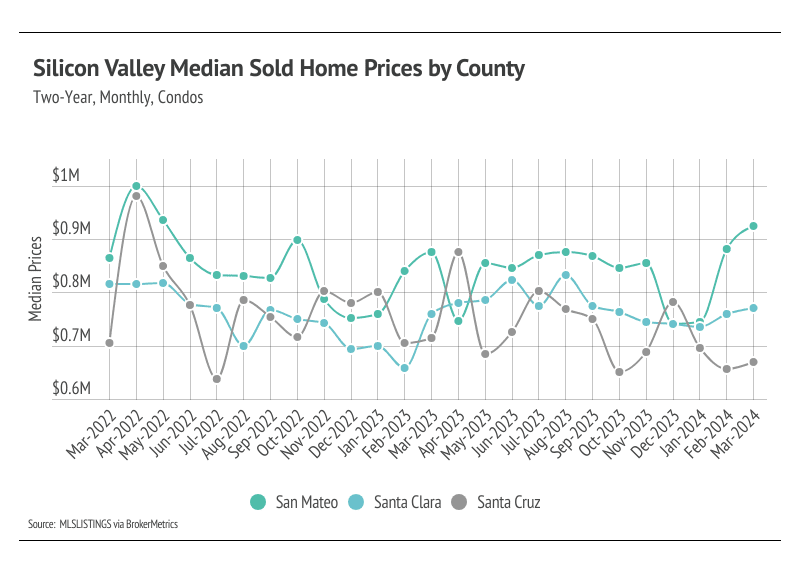

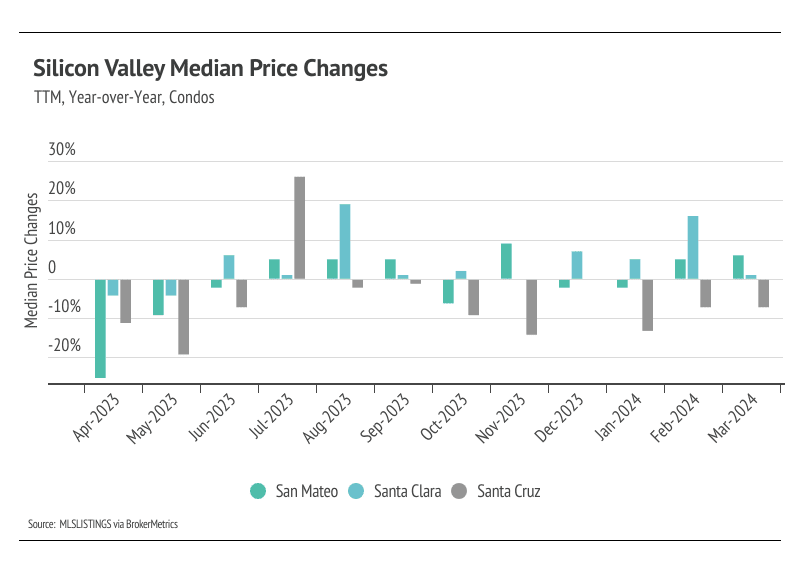

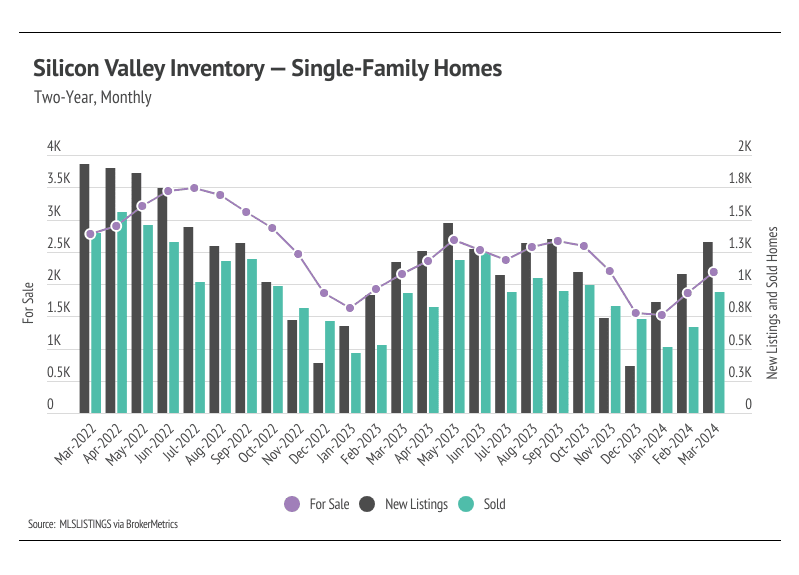

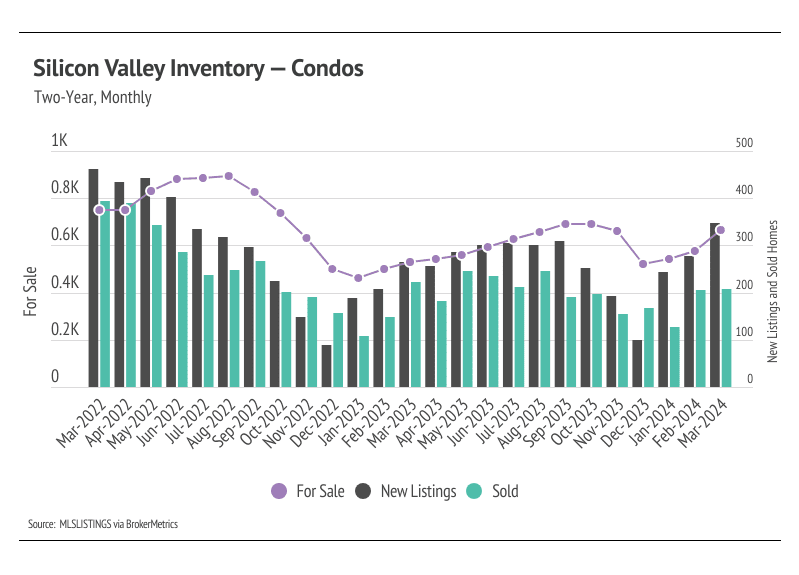

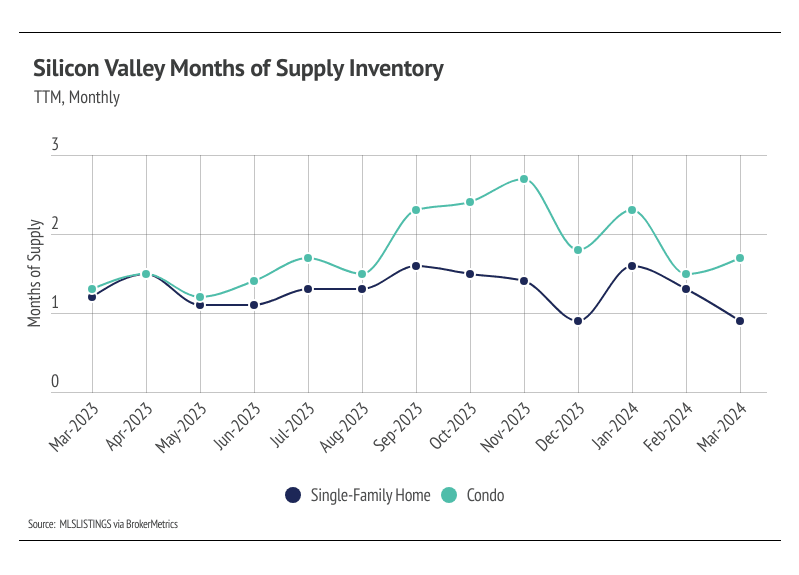

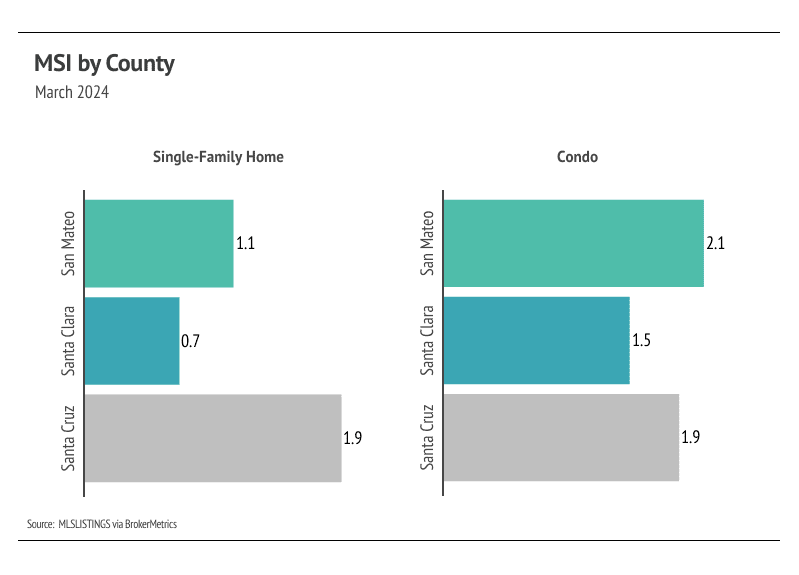

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). The Silicon Valley market tends to favor sellers, which is reflected in its low MSI. MSI trended higher in the second half of 2023, but never climbed above three months of supply. In February and March 2024, single-family home MSI fell significantly, indicating the housing market strongly favors sellers. For condos, MSI rose in March but is still quite low, also implying a sellers’ market.

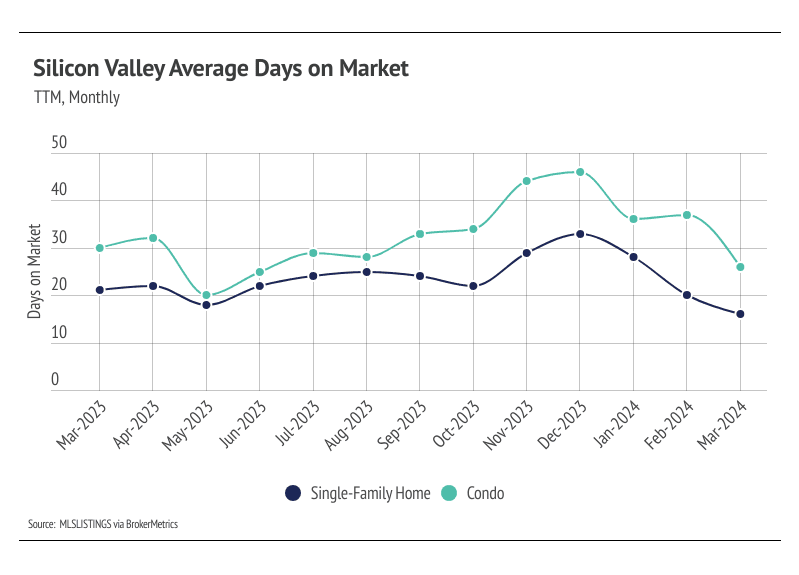

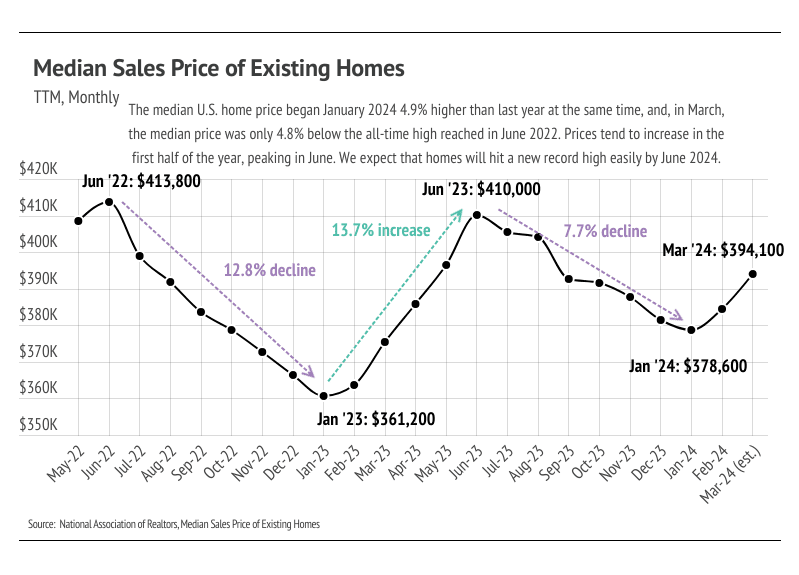

We can also use percent of list price received as another indicator for supply and demand. Typically, in a calendar year, sellers receive the lowest percentage of list price during the winter months, when demand is lowest. Winter months tend to have the lowest average sale price (SP) to list price (LP), and the summer months tend to have the highest SP/LP. In Q1 2024, SP/LP was 6% higher than last year, meaning we expect sellers overall to receive a higher percentage of the list price throughout all of 2024 than they did in 2023.

Trends, prices, and insights shaping Silicon Valley housing this winter

Trends, prices, and insights shaping Silicon Valley housing this fall

You’ve got questions and we can’t wait to answer them.