By Nil Erdal

If you’re a thriving young professional looking to move to an upbeat city with a diverse community and tons of job opportunities, it’s almost certain that the Bay Area has come across as one of your prime options. Niche.com evaluated 232 U.S. cities in order to find the most suitable cities for millennials across the nation and not surprisingly, four Bay Area cities made the top 20 list (#4 – San Francisco | #9 – Berkeley | #15 – Sunnyvale | #20 – Santa Clara). Some factors that were considered in the evaluation were ease of commuting, the percentage of residents age 25 to 34, the percentage of millennials that moved to the city in the past year, crime, median rent, ethnic diversity, and unemployment. The ranking also values quality of life considerations, such as proximity to bars, coffee shops and restaurants. Young professionals are always looking for a healthy work-life balance, and the Bay Area is clearly accommodating to those needs.

As real estate agents in Sunnyvale, we’ve been noticing a spike in interest from millennials about the home buying process within the past year. 20.4% of Sunnyvale’s population is comprised of 25-34 year olds, so it doesn’t come as a surprise to us that millennials are looking to lock down some prime real estate properties. Although Bay Area residents earn some of the highest wages in the nation, our real estate markets rank among the least affordable for both middle-class and millennial homebuyers. The reason being that in high-income regions, wealthy homebuyers have the ability to overbid and drive up prices, shutting out those on the other side of the wage spectrum. Buried in student debt or beholden to flat wage growth, many millennials are late to launch careers, marriage and parenthood, the markers that historically coincide with homeownership. We’re not going to lie and tell you that it’s going to be an easy route to homeownership as a millennial in the Bay Area. However if you love the city as much as we do and can’t see yourself settling down anywhere else, we’re here to help make the American dream a little more reachable for you. Think about how high rental costs are in the Bay Area and how you could be using that money to pay off the mortgage on your new home instead of putting it in the hands of your landlord, in order to fuel your steps toward homeownership. And use these seven tips to guide you towards some feasible options for affording your new home.

1. Be Flexible

Whenever a millennial reaches out to us about buying a home in the Bay Area, the first thing we always tell them is they have be flexible. Some come to us saying that they have to live in the heart of San Francisco and get defeated when we tell them they’re going to need a yearly salary of $158,000 ($3,680 in monthly payments) in order to afford a median home of $841,600 with a 30 year mortgage and a 20% down payment. For most millennials, this just isn’t feasible so we always tell them to look at some other neighboring cities as alternative options. Perhaps South San Francisco (Yearly income of $128,000 for a median house of $644,700) or even Oakland which is just across the bridge (Yearly income of $87,000 for a median house of $438,900). All in all, it’s important to understand that there are a lot of great neighboring cities with decently priced homes in the Bay Area so be open minded and be clear about separating your needs versus your wants beforehand.

Please keep in mind that we never completely shut out the possibility of living in a certain city because there are times when we have wonderful homes on the market in Santa Clara or Sunnyvale for a little over a half a million. However it does require a lot of research, patience and good communication between your realtor in order to get your hands on one of these gems. Check out this list of South & East Bay cities median house price to get a feel for the higher income regions.

SOUTH BAY

City…………………..Home Price………..Income

Atherton………….. $3,000,000………….$594,000

Belmont…………… $1,157,000………….$228,000

Burlingame………. $1,300,000………….$257,000

Campbell………….. $910,000…………….$180,000

Cupertino…………. $1,497,750…………..$296,000

Foster City………….$884,000…………….$175,000

Gilroy…………………$558,750…………….$111,000

Half Moon Bay……$925,700…………….$183,000

Hillsborough………$3,375,400…………..$668,000

Los Altos……………$2,369,100……………$470,000

Los Altos Hills…….$3,424,800…………..$678,000

Los Gatos………….$1,531,500……………$237,000

Menlo Park……….$1,609,600……………$297,000

Millbrae……………$1,173,700…………….$232,000

Milpitas…………….$748,600………………$130,000

Mountain View….$1,075,100……………$192,000

Pacifica……………..$733,600………………$132,00

Palo Alto…………..$2,235,000……………$442,000

Redwood City……$892,000………………$176,000

San Bruno…………$678,000………………$134,000

San Carlos…………$1,259,900……………$249,000

San Jose…………….$635,200………………$126,000

San Mateo…………$856,200………………$169,000

Santa Clara………..$768,700………………$152,000

Saratoga……………$1,600,000…………….$317,000

S. San Francisco…$644,700……………….$128,000

Sunnyvale………….$935,750………………$185,000

Woodside………….$3,088,400…………….$612,000

EAST BAY

City……………Home Price…….Income

Alameda……. $677,950…………. $134,000

Albany……….. $670,000…………..$133,000

Berkeley…….. $810,250…………..$160,000

Castro Valley..$584,750…………..$116,000

Concord……….$434,250………….$86,000

Danville………..$986,750………….$195,000

Dublin………….$609,000…………..$120,000

El Cerrito……..$619,000……………$122,000

Fremont………$711,250……………$141,000

Hercules………$405,000……………$80,000

Lafayette……. $1,227,500…………$243,000

Livermore…….$599,575……………$119,000

Martinez……….$435,550……………$86,000

Moraga…………$880,000……………$175,000

Newark…………$575,000……………$114,000

Oakland………..$438,900……………$87,000

Orinda…………..$1,300,000…………$243,000

Piedmont………$2,050,000…………$395,000

Pinole……………$389,000…………….$77,000

PleasantHill……$552,000……………$109,000

Pleasanton…….$794,750…………..$157,000

San Leandro…..$434,325…………..$86,000

San Ramon…….$783,000…………..$155,000

Union City………$552,500………….$109,000

Walnut Creek….$607,450………….$120,000

2. Think About Renting

If you’re set on purchasing a house that’s a little more than what you can afford, you could always consider the option of renting out a room to offset the mortgage. There’s a bunch of young professionals looking to rent out rooms that understand the high costs of living in the area who are willing to pay anywhere between $800 – $1500/month for a room. So if you’re looking to make more money down the road and just need a few extra bucks a month to get the house you’ve been wanting, really consider renting out that spare room. If you’re the type that likes consistently, you can rent the room on a month to month basis and have yearly contracts. Or if you’re comfortable with opening up your home to different travelers passing through the area, you could list the room on Air BnB and make a few extra bucks by charging nightly rates. You’ll probably make more from a nightly rate on Air B&B, but the downfall is that you’re going to have to put more work into keeping up with your listing and cleaning up after the visitors who come through your home. All in all, it’s an option that’s favorable to most millennials who can’t quite afford their home just yet. However we always remind our buyers to not rely so heavily on the rental income and to be comfortable with the monthly payments before signing for the house because you definitely don’t want to be stuck with payments you completely can’t afford.

3. Put that Tech Brain to Work

The advantage millennials have over any other generation competing in the housing market is that they are ridiculously comfortable with technology. So while the rest of us Gen X folks are still struggling to figure out how video chatting works, millennials are off creating 3D video recording and coming up with high tech mobile applications. Being handy with technology and keeping up to date with the latest tech trends can get you a lot further than you think in today’s real estate market.

Everyone with a smartphone has access to a bunch of mobile applications that are designed to make the home search process easier (and we’ll cover what some of these apps are in another blog). However some of the more useful apps just won’t be beneficial to the older generations. For example,

Doorsteps, an app designed in a similar fashion to the popular dating app amongst millennials known as Tinder. The concept of this app is that you swipe left to pass on a property and swipe right to save it for later. All of your saved listings get synched with your Doorsteps.com account, so you can share it with your friends and co-searchers, along with notes. So right off the bat, millennials have a strategic advantage by already being familiar with how to use the app and having more peers to engage and share listings with. So our advice to millennials out there is to find out what the most useful apps for home buying are, and use them strategically. Create a community online with fellow peers so that you can share tips with each other and be the first one notified when a property that matches your criteria hits the market.

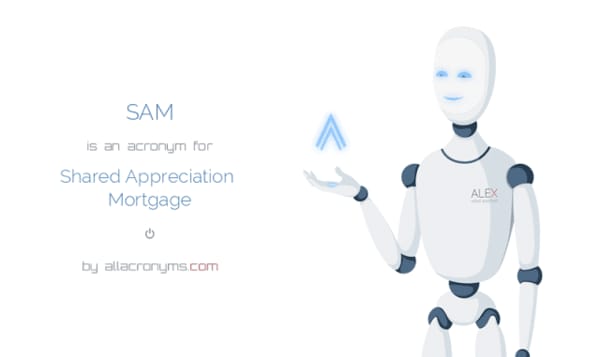

4. Consider a Shared Appreciation Mortgage (SAM)

Under this arrangement, your family, friends, or even a third-party may buy a portion of the home and share in any appreciation when the home is sold. The owner/occupant usually pays the mortgage, property taxes, and maintenance costs, but all the investors’ names are usually on the mortgage. So for example, let’s say you purchase your home for $500,000 where the lender and borrower agree to a lower interest rate of 5% instead of 6%. The borrower puts down $100,000 and takes out a mortgage of $400,000 amortized over 30 years. Because of the lower interest rate, the monthly payment is reduced from $2,398 to $2,147. However, this saving in monthly payments comes with a trade-off. Suppose the property is later sold for $700,000. Because of the agreement on the contingent interest of 20%, the borrower must pay the lender 20% of the profit, namely, $40,000. By participating in the appreciation of the property, the lender takes an additional risk that is related to its value. Hence, whether this is a favorable trade-off depends on the conditions of the housing market. Millennials looking to purchase a home in the Bay Area might come out favorable for this type of arrangement since home values are expected to increase drastically over the next few years. There are companies available that can help you find such an investor, if your family can’t participate.

5. Explore Seller Financing

In seller financing, the seller takes on the role of the lender. Instead of giving cash to the buyer, the seller extends enough credit to the buyer for the purchase price of the home, minus any down payment. The buyer and seller sign a promissory note (which contains the terms of the loan). They record a mortgage (or “deed of trust” in some states) with the local public records authority. Then the buyer pays back the loan over time, typically with interest. Seller financing can be a useful tool in a tight credit market. It allows sellers to move a home faster and get a sizable return on the investment. And buyers may benefit from less stringent qualifying and down payment requirements, more flexible rates, and better loan terms on a home that otherwise might be out of reach. Typically sellers that have their own mortgage paid off are more inclined to an agreement like this. However, it may be an option that you wouldn’t have known you had unless you asked.

For more information on how to afford a home in the Bay Area, Contact us today.